We hope this update finds you and your families safe and well.

At CrowdProperty, we believe in bringing you, our lenders, the very best residential property project lending opportunities (quality projects being undertaken by quality property professionals), that are always first-charge secured at modest loan to value levels having undergone our rigorous, expertise-led due diligence process. As property experts, we then work closely with our borrowers throughout their projects to maximise the likelihood of a successfully completed project, in the best interests of your investment. These elements are all key to our exemplary track record and a major contributor to ongoing site activity and paybacks through the Covid-19 period – for example the £1,766,159 project payback on Friday that included £166,159 of interest.

We fully recognise that it has been difficult getting into loans recently. The last 10 funded projects, totalling almost £3m (at average loan to gross development value of 52.4%) have each funded in 55.1 seconds on average. It’s important to note that we will only launch new projects onto the CrowdProperty platform that are both ready for funding and meet our lending criteria at that time, which have naturally tightened of late.

In this update, we will go into the following by way of reflection and update:

- A brief recap about why CrowdProperty exists and how it benefits everyone as well as the wider economy

- A deeper dive into some of the key ways CrowdProperty brings you the very best lending opportunities

- What’s going on in the property market and what might we expect going forward

- How CrowdProperty is faring during Covid-19 and why there’s a very strong outlook of bringing you more high quality lending opportunities

- A reminder on the different ways you can lend with CrowdProperty, including tax-free through the CrowdProperty ISA and SSAS/SIPP pensions

- A brief recap about why CrowdProperty exists and how it benefits everyone as well as the wider economy

Our last update went into detail on why CrowdProperty exists but it’s worth briefly recapping on the key points.

We set up CrowdProperty in 2013 to give a better deal for all – our lenders, our borrowers, the under-supplied housing market and spend in the UK economy – by more directly matching the supply and demand of capital with efficiency (enabled by technology) and effectiveness (enabled by deep asset-class expertise). Our relentless focus is on uniquely and directly originating billions of pounds of property projects and expertly curating lending opportunities with first charge security at modest LTV levels serving domestic under-supplied demand in liquid markets at mainstream, affordable price points. We’ve seen over £3bn of projects and have funded almost £70m – a conversion rate of under 3%, or otherwise put, a healthy rejection rate of over 97%. This is why institutions also want a slice of the action and are active on our platform after months of due diligence on the business, validating the strength of the proposition we’ve built for you. You can further benefit from the tax-free cherry on top via the CrowdProperty ISA and SSAS/SIPP pension lending.

- A deeper dive into some of the key ways CrowdProperty brings you the very best lending opportunities

There are many ways that CrowdProperty has built a uniquely strong, competitively advantaged business that delivers market-leading benefits to you as a lender, a few of which we’ll highlight below.

First of all, CrowdProperty has built a unique direct to developer route to market which both helps CrowdProperty to close the best lending opportunities, and brings you better rewards in the form of a greater share of what the borrower pays. Coupled with our deep expertise in exactly the asset class we are lending against and a standout, differentiated borrower proposition (as explained in our latest borrower update, which may give you interesting borrower-side perspectives), we have built a lending business ideally positioned to attract the best opportunities and deliver those returns, enabled by superior economics, superior underwriting, superior service, superior loan monitoring and superior customer retention from deeper property professional relationships.

CrowdProperty only offers first charge secured lending opportunities, which not only puts your capital and interest first in the queue in a recovery situation, but an often under-estimated benefit of first charge security is that the first charge holder also controls the recovery process. That puts your capital in the safest, most controllable position – never underestimate the risks associated of ‘security’ that is junior to the first charge.

Coupled with security is security coverage. There are three key measures to keep an eye on: Initial Loan to Value – i.e. the amount released to acquire the initial asset as a proportion of its value; Loan to Gross Development Value excluding interest – i.e. the protection of your capital; and Loan to Gross Development Value including interest – i.e. the protection of your capital and interest. Averages for CrowdProperty come in at 61.2%, 53.1% and 58.9% respectively, relative to values where there is always demand and has been under-served for years - domestic under-supplied demand, in liquid markets, at mainstream, affordable price points. This means that there is, on average, 38.8% of initial value buffer, 41.1% end of project buffer to repay both your capital and interest and a 46.9% buffer protecting your capital. One thing that Covid-19 highlights is that anything can happen, so be sure that your investments are well protected.

Such statistics then bring us on to transparency. Those risk exposure figures are all outlined very clearly for every project and on our award-winning statistics page. Transparency is critically important in this sector and you should insist on it… where things aren’t sufficiently clear, there’s probably a reason for it. We’re fully transparent about our performance through clear disclosure and also by opening up our loan book – and every cashflow therein – to various market commentators including leading market analyst Brismo. This underlines our complete commitment to disclosure best-practice and independent accountability for the performance of every loan that we originate, both historically and going forward.

In those statistics, you should be clear about whether you are getting your fair share of the returns. Laid out on our statistics page, it’s made clear that we take a 2% points spread between the interest rate we charge borrowers and the interest rate we give to lenders. This number is critically important. If you’re being offered 8% and the borrower is paying 10%, it’s a far fairer and safer position than getting 8% when the borrower is paying 15%. Why? The borrower could not borrow cheaper from elsewhere, is likely to be significantly more risky and the platform is not passing on a good proportion of the returns to those bearing the risk. We’re a lender of first resort to compete for the best projects so have competitive borrower interest rates, and we have built a very efficient and effective system to deliver as much of those returns to you as possible. If platforms aren’t entirely transparent about the spread between borrower and lender rates (and the vast majority aren’t), there’s definitely a reason why.

Finally, you’re only a lender if you get the money back – otherwise you’re a charity without a cause. The critical thing in lending is intimately knowing what you’re lending to, which is right at the heart of CrowdProperty. Deep expertise in exactly the asset class we’re lending against sits at the core of what we do with decades of hands-on experience in what the borrowers are doing, through multiple economic cycles. This not only gives us the edge in securing the best projects, offering property finance by property people, but also the critical advantage of knowing how best to solve problems and reach successful conclusions of projects, to safeguard your capital. What’s more, having been lending since 2014, we believe in absolute focus. Lending to small and medium sized property professionals undertaking quality property projects is not part of what we do it is the only thing we do. You don’t see Tiger Woods playing much tennis – we believe that it’s focus that makes us World Class and that’s how we’re the UK’s leading specialist property project online lending platform.

- What’s going on in the property market and what might we expect going forward

There’s a great deal of discussion in the media about the outlook for the property market. Dramatic headlines about huge falls in the market are referring to transaction volumes of course, with the lockdown having had a huge impact on the ability to agree and complete sales during this time. The sales and lettings markets have opened up again and the many transactions that have effectively been on hold will start to progress once more, actively encouraged by The Government as restrictions start to ease in planned ways. Building and construction has always been sanctioned to continue in the UK throughout Covid-19 if it could be done safely (in every way - on-site, supplies delivery, transport to site etc) and it is now being actively encouraged to reopen fully.

Stepping back however, evidence from previous pandemics suggests a short, sharp trough (as discussed in this article from Zillow Research) and then a reversion to the underlying trend leading into the pandemic. We know that after a few years of political uncertainty, the UK voted in a strong majority government, resulting in a decisive direction on EU membership, bringing with it stronger foundations in markets including the property market. This played out in robust property market data in early 2020 in terms of transaction volumes, strengthening prices and RICS property professional surveys’ market lead indicators.

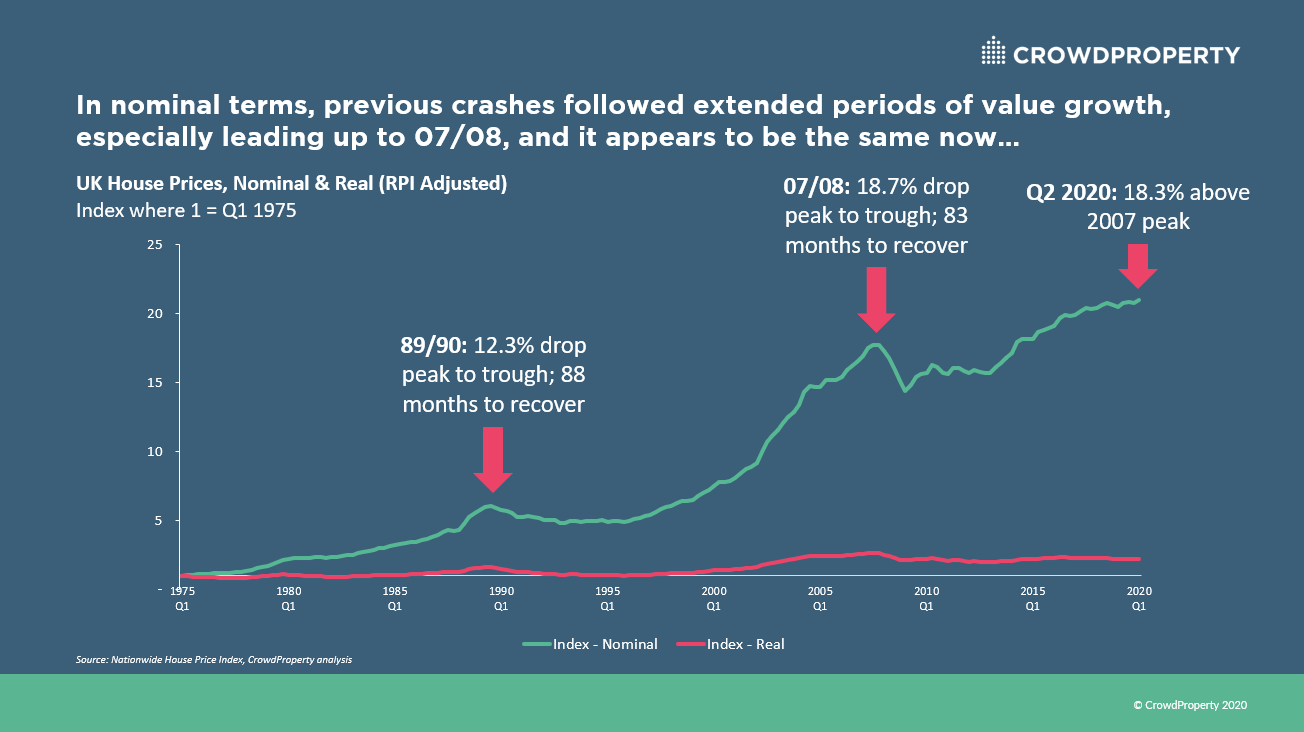

Before we look forward at the forward-looking supply/demand balance, let’s look back to guide us on whether this shock could spark a long-awaited correction. This has been evident in the past – both 89/90 and 07/08 experienced long periods of housing market growth before those economic shocks drove double-digit percentage declines (18.7% in 07/08 vs commercial property dropping 43%), taking years to recover. In the below chart, showing the Nationwide House Price Index since 1975, this can clearly be seen and at first glance, one might think the signs are here again:

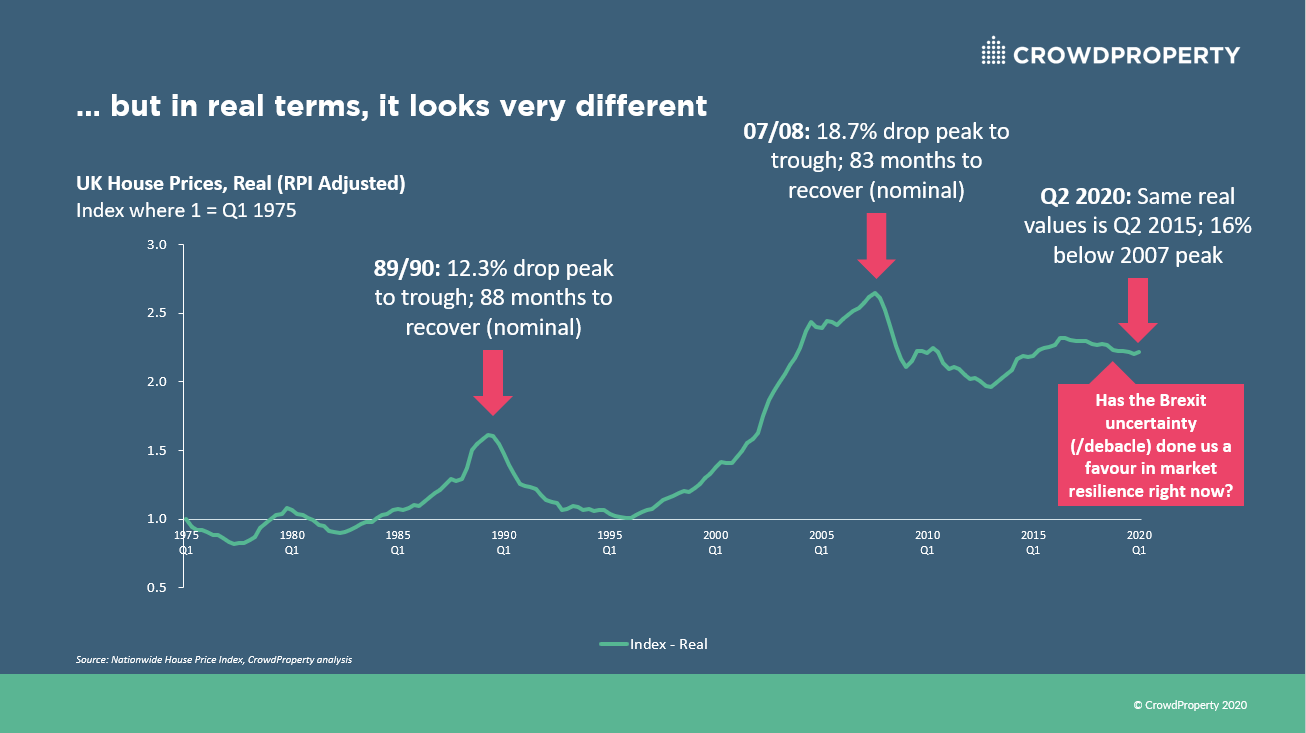

But this is where it is critical to separate real from nominal growth. In other words, let’s take the effects of inflation out of the nominal (unadjusted for inflation) data. In the above chart, the green line shows the Nationwide House Price Index in nominal terms, whereas the pink line shows it in real terms, adjusted for inflation (RPI-adjusted). This reflects the real value growth in UK housing. Clearly on the above chart, it’s difficult to see the movements (although interesting to note the extent of the difference), so below shows just the Nationwide House Price Index in real terms:

This shows a very different story to the nominal picture – average values today are 16% below the 2007 peak, have been pretty much flat since early 2015 and are currently the same as in late 2010 values. This is a very different context to the extended periods of high growth in values that led into the 89/90 and 07/08 market falls.

Every market cycle is different of course. Whilst it’s also important to keep in mind that this situation is not a result of failings in the financial system and therefore mortgage debt liquidity expected to return more swiftly, there are still significant uncertainties.

On the demand side, medium/long-term unemployment is the biggest unknown, with the Government acting proactively with arguably world-leading measures to protect jobs such as the Job Retention Scheme. Ultimately, the impact on people’s household finances and job security will determine the predominant level of underlying demand. Somewhat counteracting this on the demand-side is pent up demand from lower transaction volume through the Brexit uncertainty and through 2020 to date, affordability supported by historically low BoE base rates and most likely a swifter return to a normal mortgage market than previous market falls.

On the supply-side, whilst unfortunately there will be many more probate listings this year, there will be a greater decrease in construction completions in 2020, which has been under-supplying the market for decades. More materially, given the nature of shorter-term market expectations, many would-be sellers will hold off from listing their properties onto the market. As in any market, there will be those that need to sell, but those with discretion on when to sell will naturally wait for evidence of more transaction liquidity and stability in the market. This supply/demand balance is arguably much better positioned than in 07/08, where many wanted/needed to sell (including banks whose blanket repossess and fire-sale approaches exacerbated supply), but only very few could buy (due to very limited mortgage debt options) or were prepared to buy (due to long-term prospects in the debt markets holding back recovery).

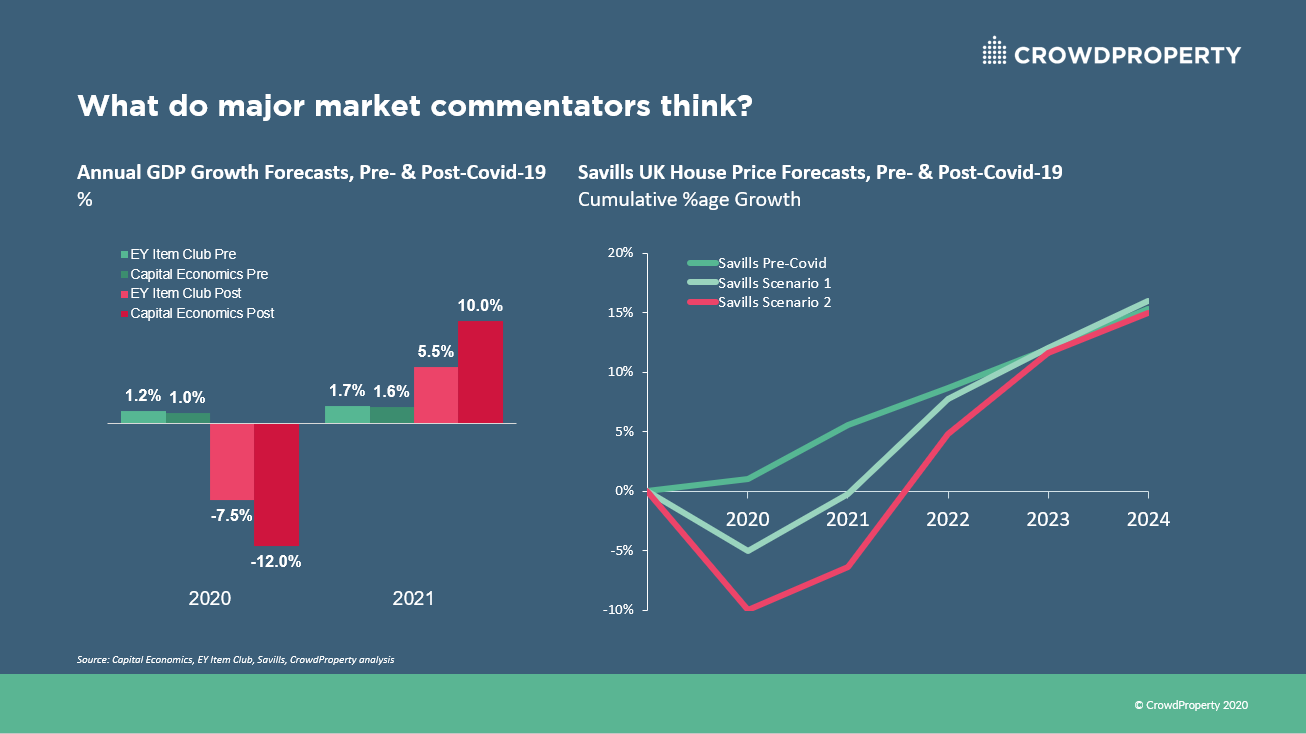

So, do market commentators agree with this view? The latest (May 2020) viewpoints of both GDP and the housing market still align to view of a significant dip in 2020 but a significant recovery in 2021:

Firstly, taking a look at GDP expectations, the anticipated decline is deep, largely driven by an expected decline of 24% in Q2 2020, i.e. the lock down period we’re right in the midst of, in Capital Economics’ view of a 12% fall in 2020. They go on to forecast a 16% growth in Q3 and 4.8% growth in Q4 2020 as the economy resumes. 2021 is then expected to recover much of the 2020 fall with a 10% bounce-back, all of which is in line with their average forecasts across the Eurozone. The EY Item Club expectations show a similar shape, if less severe in nature.

In terms of housing growth, Savills’ latest forecasts expect between 5% and 10% falls in 2020 (albeit based on lower transaction volumes – i.e. those needing to sell) with the bounce-back converging to pre-Covid-19 cumulative growth forecasts by 2023 and positive on 2019 values by 2021 (scenario 1) and 2022 (scenario 2).

Ultimately, nobody has a crystal ball and therefore you should protect your downside, for example with first charge security at modest loan to value levels, serving domestic under-supplied demand, in liquid markets, at mainstream, affordable price points – where there is always demand which has been under-served for years, as per CrowdProperty’s sole and absolute focus. It’s important to note that we will only launch new projects onto the CrowdProperty platform that are both ready for funding and meet our lending criteria at that time, which have naturally tightened of late.

- How CrowdProperty is faring during Covid-19 and why there’s a very strong outlook of bringing you more high quality lending opportunities

CrowdProperty is faring very well during Covid-19 times. Whilst we’ve significantly tightened our criteria, our strong direct route to market enables us to work with prospective borrowers to make sure that everything is ready, all elements are very well risk managed, and that in some cases they have more equity capital to put into the project. Continuing to lend means that we are further enhancing our reputation amongst our target borrower market, at a time when other funders, with concentrated sources of capital that are exposed to equity market volatility, are stopping lending, reneging on offers and even refusing mid-project drawdowns. Many are destroying their reputations when it really counts, which means that in the short, medium and long-term, we will attract more and more applications, from which we can continue to curate the best, to offer to you.

As previously communicated, almost all of our current projects have continued on site because of our concentration away from London, in locations that are less reliant on public transport and as they are generally lower density sites that are smaller in size than many, have fewer people to define and implement safe operating procedures with. We are reviewing projects on a case by case basis, continuing to carefully assess drawdown requests and independent monitoring surveyor reports, releasing drawdowns only where validated progress has been made. As required we will continue to raise funds for follow on project phases when site progression is clear but it’s important to note that funds are only ever released upon independent review of completed elements of the project, funded in arrears to the progress and the value that has been added on site. There will be some cases of delays, most frustrating of which are those which are fully finished projects awaiting refinance or sales, but rest assured that we are working closely with all borrowers, in your best interests, with ample security cover in place. It is all parties’ best interests to complete and exit the projects, so everyone is aligned to the ultimate goal of returning your capital and interest, and as we work through the best solutions for that goal, we will communicate as appropriate. Right now, more than ever, is when the importance of a knowledgeable funding partner is critical and having been in the shoes of developers ourselves, we can work at a uniquely practical level with borrowers through this. This benefits existing loans and the long-term lender brand we are building with property professionals, meaning more quality projects for you.

On the lending side, as you will have experienced, the last 10 projects have funded in less than a minute on average. We recognise this can be frustrating. We have a strong pipeline that we’ll launch when it’s right for those projects and we’re working hard to bring you more. We only grow in two ways – growing our origination (overall application rate) and increasing the quality mix of that origination. The factors laid out above are meaning that we are seeing more and more projects day by day, but we will only ever list projects that meet our only ever tightening criteria as a quality-first lender and we do not set hard targets internally, nor incentivise staff on lending volume, as that can drive misaligned behaviour.

The capital position on the platform has rarely been stronger and we’re certainly not considering cutting rates, stopping withdrawals and/or introducing lender fees to get lenders to subsidise our operations as some platforms have. Our absolute focus has always been building a long-term trusted brand with a resilient and sustainable business model throughout market cycles, which we are proving right now. The financial health and sustainability of the business is important to all stakeholders. Our non-London cost base ensures that we can have greater resource for our spend, whilst ensuring that we have access to strong capabilities in the large yet less competed Birmingham talent pool. It short, we get more bang for our buck which contributes to building a very efficient and very effective lending business. Furthermore, all our functions (other than societal-bound professional services such as formal valuation surveying and conveyancing) are in-house, under the same roof for upmost control, security, responsiveness, consistency and culture. We have a brilliant team and despite the wider market and economic context, April was and May will be both profitable and cashflow positive for CrowdProperty, proving the robustness and sustainability of the business.

- A reminder on the different ways you can lend with CrowdProperty, including tax-free through the CrowdProperty ISA and SSAS/SIPP pensions

We are continually improving the lending products we bring you, including the ever-evolving AutoInvest and the numerous tax-free ways of lending.

The very popular CrowdProperty ISA enables you to use your annual tax-free ISA allowance and to transfer existing ISA balances into a segregated wallet in your account to lend with CrowdProperty. Similarly, millions of pounds of pension money from both SSAS and SIPP pensions has been lent to CrowdProperty projects.

CrowdProperty AutoInvest is a stress-free way to invest money across every high-quality, first charge secured project we launch on the CrowdProperty platform, helping you build a diversified loan portfolio. AutoInvest is now also available for SSAS/SIPP pension lending accounts and offers the ability to AutoReinvest payback capital and/or interest (including paybacks from SelfSelect pledges now) and invest regularly through EverydayInvest.

We get a lot of questions in particular about the AutoInvest algorithm which has evolved into a complex piece of code given the many to many permutations and requirements by account type. Crucially, the AutoInvest algorithm treats everyone fairly, based on the supply of projects, the demand from AutoInvestors and your AutoInvest settings. Everyone receives the same proportion of their desired maximum in each project and the overall AutoInvest allocation into each project gives those who SelfSelect a fair proportion too.

We’ll continue to share information and our latest thinking via our blog, where you can also find our series of 40 articles covering all aspects on alternative finance, peer-to-peer lending, property and CrowdProperty. As we don’t share all of our analysis, thinking, research and views over email, if you’re interested in keeping in closer touch, do also follow us on social media at LinkedIn, Facebook, Twitter and Instagram.

We’re building the best property project lender in the market to attract the very best lending opportunities, which we scrutinise, present, secure and monitor for you, our lenders. We take a long-term, strategic perspective on the business to ensure that it is robust and sustainable through all market cycles and that we continue to deliver exceptionally for all our customers.

Insist on the best and together we build.

Keep safe,

Mike Bristow (CEO & Co-Founder) & Your CrowdProperty Team

As featured in...