We recently looked at our virtuous circle in property lending. Below we get forensic on how we stress test our loan book, and the next post overviews the sources of our loan capital.

We recently looked at the importance of first charge security in protecting your capital. For this to provide a meaningful safety net, however, any claim needs to be on high-quality assets, able to retain their value in times of market stress.

Of course, the preferred option is for no defaults. Economies work in cycles, however, and indicators are pointing down. When the economy turns negative, default rates can turn positive. Many wealthy investors are already responding by hoarding cash, despite the fact that, in real terms, they’re losing out after inflation has taken a bite.

Such reticence is understandable: having inflation erode your savings at a couple of percentage points a year is better than seeing about 40% wiped out over a similar period, which is what happened to stock markets in 2008/09.

An investment that goes up like a rocket and down like a stick is no investment at all. CrowdProperty therefore does everything it can to ensure that our loans – both the back book and new approvals – are as weatherproof as possible.

The best way to test our portfolio is to try as hard as we can to break it – virtually, of course. It’s like the financial equivalent of crash test dummies.

How do we do this? Over the past three decades, two recessions (2007-09 and 1989/90) have been linked to residential property, with significant negative effects on its valuation. We’ve put our loan portfolio through a stress test that matches – indeed, goes beyond – both, to gauge the impacts. (Note that publishing a resilience test is part of the best practice criteria of leading industry body, the Peer2Peer Finance Association. If you come across a platform that doesn’t do this, it’s worth asking why.)

At the trough of the 2007/08 crisis, UK house prices dropped on average 18.7%, to March 20091, and took until August 2014 to recover to the same level2. In the trough of the 1989/90 crisis, house prices dropped by 12.3% and took until January 1997 to recover. Our analysts applied these conditions to our loan book, at a granular geographic level, to determine what economic conditions would compromise the security underpinning our loans. More details are given in this report (available to those with a CrowdProperty account)

Importantly, the implications from these tests have been built into the loan appraisal assessment, to ensure the portfolio’s increasing resilience.

So, let’s look through the results.

We ran three different scenarios, reflecting progressively worsening market events.

In Scenario A, we applied a repeat of the 2007/08 crisis onto our complete loan book. We looked at how our loan book would be impacted at the end of the loan term, six and 12 months post loan term, and during the trough of the crisis. Granularity was at a local authority level and we split data by property type, so we just see a high-level average, but understood local and sub-sector effects.

Here, not a single loan on our loan book passes 100% owed at exit to GDV at any point. That means if we had to take possession of the development to redeem our lenders’ capital, that capital would still be fully covered.

The average owed at exit to GDV percentage assessed before launch was 58% across our entire loan book. In this scenario, the average owed at exit to GDV was 69% at the end of the loan terms, 71% at the six months post loan term position, 72% in the 12 months post loan term, and 67% during the trough of the crisis. The highest owed at exit to GDV percentage was at 98% on a historical loan that has already been paid back in full.

Scenario B is a more severe version of scenario A, combining a more severe version of the stagnation in house prices after 1989/1990 with a decline of the same magnitude as 2007/08 – the absolute worst of both worlds. Here, two of our historical loans exceeded 100% owed at exit to GDV, both of which have already paid back in full. One of these two loans was in 2015, very early in the lifetime of CrowdProperty. If this loan was funded today, we would offer less to the borrower, as our lending criteria have tightened since 2015 – and, as a policy, only ever tighten.

With our current active loan book, not a single loan exceeded 100% owed at exit to GDV in the 12 months post loan term position. The average owed at exit to GDV percentage with the adjusted GDV values across our entire loan book were: 71% at the end of the loan terms, 75% in the six months post loan term position and 78% in the 12 months post loan term position.

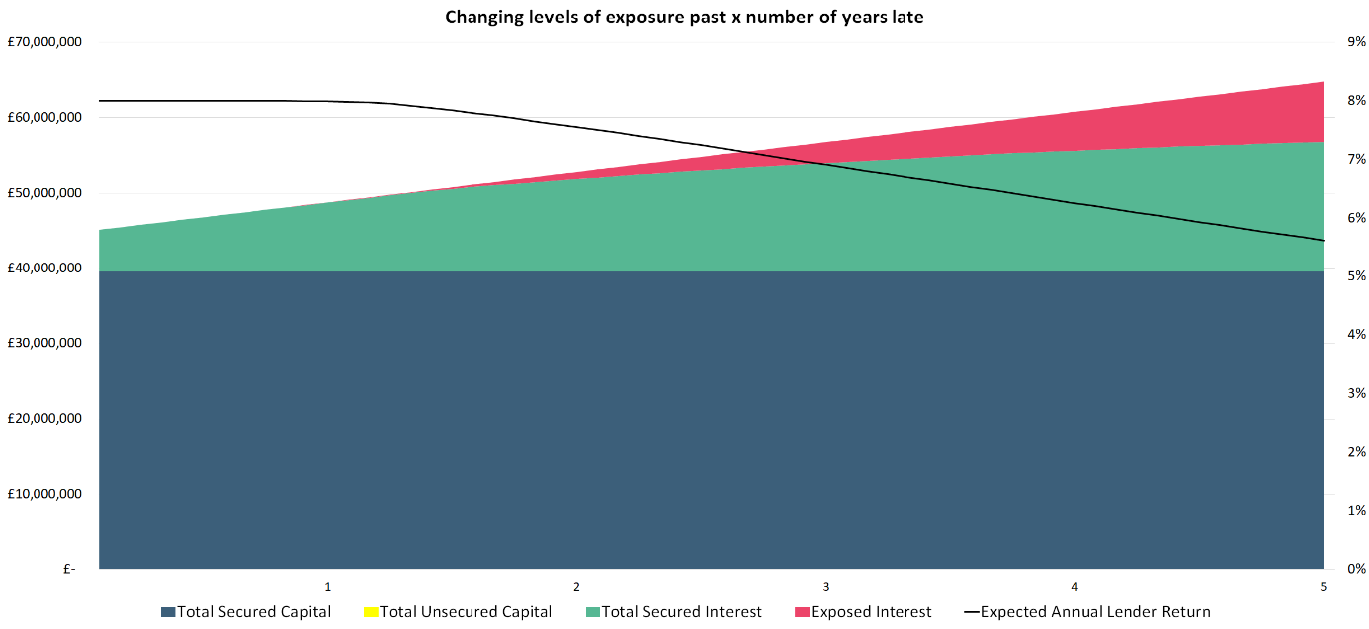

The final scenario – C – is a continuation of scenario B and is a test of how long our loan book could last under the conditions imposed under scenario B, by calculating the level of exposure on both interest and capital as well as calculating the expected lender returns.

Scenario C shows the exposure of our loan book, assuming all of our loans went late at the same time, in the same adverse conditions of scenario B where GDV values are adjusted accordingly. Including a measure of expected lender returns, adjusted for exposed interest

As the graph shows, total lender capital would never become unsecured and lenders would maintain a return of their capital between 8% and 5.5% even when our loans have accrued unsecured interest at a period of five years late.

Our Property Director Andrew Hall believes it would take us, in a worst-case scenario, a maximum of 12 months past loan end date to sell a property at market value. The breakdown of this would be: a 45-day period, where the borrower is given time to sell the property; a 90-day legal process to exercise our first charge security; and a maximum of six months to sell the property.

We monitor our loans closely and are therefore aware of any that may go late well in advance of their due date, through a wide array of market data and continuous communication with the borrower throughout the project.

In addition, we are mindful of the vulnerabilities of the market on a forward-looking basis, specifically, where it looks vulnerable to a correction. In current market conditions, that means not focusing on macro-economically sensitive areas, such as prime central London, which are considerably more volatile and less dependent on predictable supply and demand fundamentals – it’s a market that’s really about a few foreign buyers, which are inherently unpredictable, rather than mass domestic demand. Instead, we back projects supplying fundamental domestic demand, under-supplied for decades, at mainstream property end-values.

While it’s true that past performance is no guide to the future, we have combined the worst of all historic worlds (short of tracking back to the Black Death) against our portfolio, and factored in the lessons from this into our loan selection, to make sure the portfolio is strong now and can only get stronger.

Find out more at www.crowdproperty.com

Read more about how investing works and investment options at www.crowdproperty.com/lenders

View our statistics page: www.crowdproperty.com/statistics