Article 6 in a series of 40 articles on P2P, Property and CrowdProperty

In article 5, we explained the importance of transparency. This delves into what you can learn from decent disclosure – the important metrics – and next we explain our due-diligence processes.

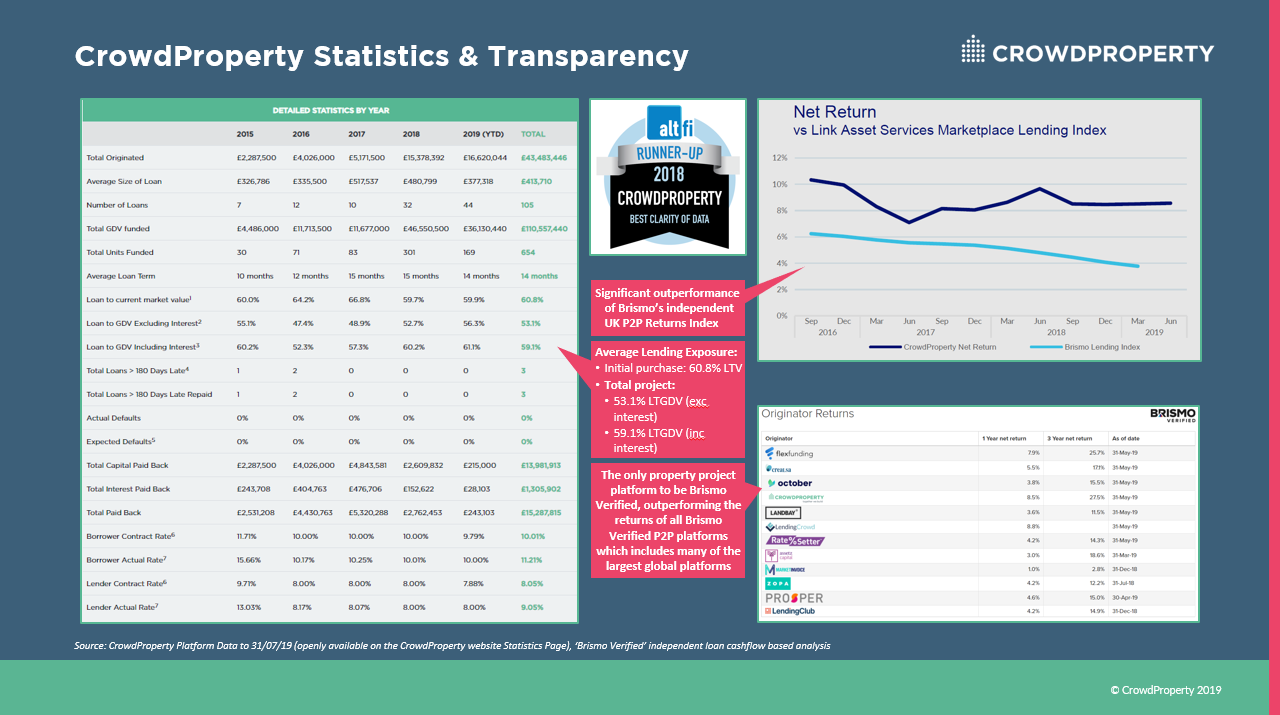

In the last article we explained why it was so important that a lending platform publish its numbers and how we lead the market in this respect. In this piece, we’re going to look in greater detail at what those number are, what they tell you and why they matter.

We are, we confess, data geeks. While you might not want to get stuck in a lift with us, our obsession with the numbers underpinning our business and the lending we approve means that you have an assurance that we are monitoring every aspect of our loan book to ensure that it is as robust as is possible and being held to account for its performance.

So, by way of example, here are some numbers that we are rather proud of.

CrowdProperty has funded the development of more than £100m of property and over 600 homes, by lending more than £40m across over 100 projects since we formed the business in 2013. Not only is that funding much needed housing supply, but also adding value to UK housing stock (over £60m) and increasing spend in the economy (over £30m on labour, materials and services). Over that time, we have a 100% capital and interest payback track record – more than £15m and counting. That means all of our nearly-8000 lenders have got the cash they anticipated back, including the interest.

Important metrics

The reason we’ve been so successful is that our award-winning clarity of data also goes in to a few more, very important numbers. Some of the important statistics we look at are explained below.

Loan-to-value (LTV): Remember the scary LTVs before the financial crisis – sometimes 100%-plus for first time buyers? That really is worrying, because the higher the LTV, the greater the risk, all other things being equal. A lower LTV means that proportionally more real assets back a loan. If it defaults, the lender therefore has a bigger pot of assets to call on in order to reclaim both the capital and interest accrued. More than 100% means there’s no way, even in the best of circumstances, you could get all your money back in the event of default.

Our average loan to current market value – which is the value of the current asset before anything is done – is 60.8%. What’s more, CrowdProperty will only work up to certain LTVs, and each project must meet our rigorous 57-step due diligence criteria that looks at every number associated with the project.

There are other metrics, similar to LTV, that provide further perspective of a lenders’ risk (if only 1 number could say everything) – specifically loan to gross development value. In property development, LTV needs to be considered alongside the loan to gross development value (LTGDV), which is the final estimated value once the project has completed. Breaking this down:

GDV = Land + construction + fees + profit

Land = Purchase price of land/property/site acquisition

Construction = Building and construction costs

Fees = Fees, transaction and finance costs

Profit = Developer’s profit

We then provide two LTGDV measures: LTGDV excluding rolled-up interest (average to date is 53.2%) and LTGDV including rolled-up interest (59.1%). Whether or not the GDV is achievable over the defined development period is of vital consideration through our detailed due diligence covering both the numbers and wider elements of project risk (that’s why proper property expertise is more than just spreadsheets).

Other data points on our statistics page then open up on how many materially late loans we’ve had (by FCA and P2PFA definitions), the number of projects funded, the amount paid back (the ultimate proof of lending track record) and the average rates to both borrowers and lenders, implying the platform spread, the great importance of which we discussed in Article 5. In brief, it’s critically important to understand the risk that your capital is bearing, which is best proxied by rate that the borrower is paying (as that’s market driven), and how much of that you are getting. Looking at the loan contract rates shown on our statistics table, the average borrower contracted interest rate is 10.01%. The average lender contracted rate is 8.05%. The average ‘spread’ to CrowdProperty is under 2% – i.e. we work extremely hard to make our business costs as low as possible to give you as much of what the borrower pays as possible. ‘Actual’ borrower and lender rates are then ever so slightly higher – this average reflecting the slightly higher rates paid by the borrower and paid to the lender in the cases where a loan has run late. It’s critical to understand these figures for any platform (whether direct lending or where your capital goes into a ‘pot’)… and in an industry that has a founding ethos of transparency of risks and rewards, it’s rarely made as clear to you as it should be.

Lastly for now, it’s important to highlight that we secure ever loan with first charge security. That means that if the borrower defaults, we can repossess those assets and fully control a recovery process in order to repay our lenders’ capital and interest. We’ll talk about this a few times through this series of 40 articles, because it’s fundamentally important.

In the next article, we’ll look how this contributes to the broader imperative of how CrowdProperty protects our lenders’ capital with The CrowdProperty Shield.

Find out more at www.crowdproperty.com

View our statistics page: www.crowdproperty.com/statistics

As featured in...